Struggling with debt and considering a consumer proposal? You’re not alone. But before you make a decision, it’s important to understand how this option could affect your credit score. Will it hurt your chances of getting a loan in the future? How long will it take to rebuild? We break down everything you need to know about how consumer proposals impact credit ratings in Canada, and the steps you can take to bounce back stronger.

What Is a Consumer Proposal?

A consumer proposal is a legally binding arrangement between you and your creditors, allowing you to pay back a portion of your debts over time, usually between 3 to 5 years. Unlike bankruptcy, a consumer proposal allows you to avoid the loss of your assets while settling your debts.

Key Points of a Consumer Proposal:

- Legally Binding Agreement: Managed by a licensed insolvency trustee, it helps restructure your debt.

- Debt Relief: It reduces your overall debt burden and freezes interest, allowing you to repay what you can afford.

- Protects Assets: Unlike bankruptcy, a consumer proposal doesn’t typically result in the loss of assets (under certain conditions).

How a Consumer Proposal Affects Your Credit Score in Canada

So, how does a consumer proposal affect your credit? The short answer is: it significantly impacts your credit score, but the impact is temporary.

1. Immediate Impact on Your Credit Score

When you file a consumer proposal, it directly affects your consumer proposal credit rating. Your credit score will drop because creditors agree to accept less than what you owe. Here’s a breakdown of what happens:

- R7 Rating: Your credit report will reflect an R7 rating while you’re in a consumer proposal. This indicates that you’re in a debt settlement agreement.

- Credit Score Reduction: Most people experience a credit score drop of 100–150 points right after filing for a proposal. The exact drop depends on your credit history before the proposal.

Reddit Insight:

This thread discusses how people’s credit scores are affected after filing a consumer proposal and their experience of rebuilding their credit, which aligns closely with your article’s focus on the short- and long-term impact of consumer proposals on credit scores.

2. Duration of the Impact

Your consumer proposal credit rating will stay on your credit report for up to 3 years after completion. This means that even if you successfully complete your proposal, your credit score will be affected for that time period.

- R7 Rating Duration: After 3 years, the R7 status is automatically removed, and your credit report will no longer show the consumer proposal.

- If Defaulted: If you fail to stick to the terms of the proposal, your credit rating may drop further to an R9 rating, signaling non-payment.

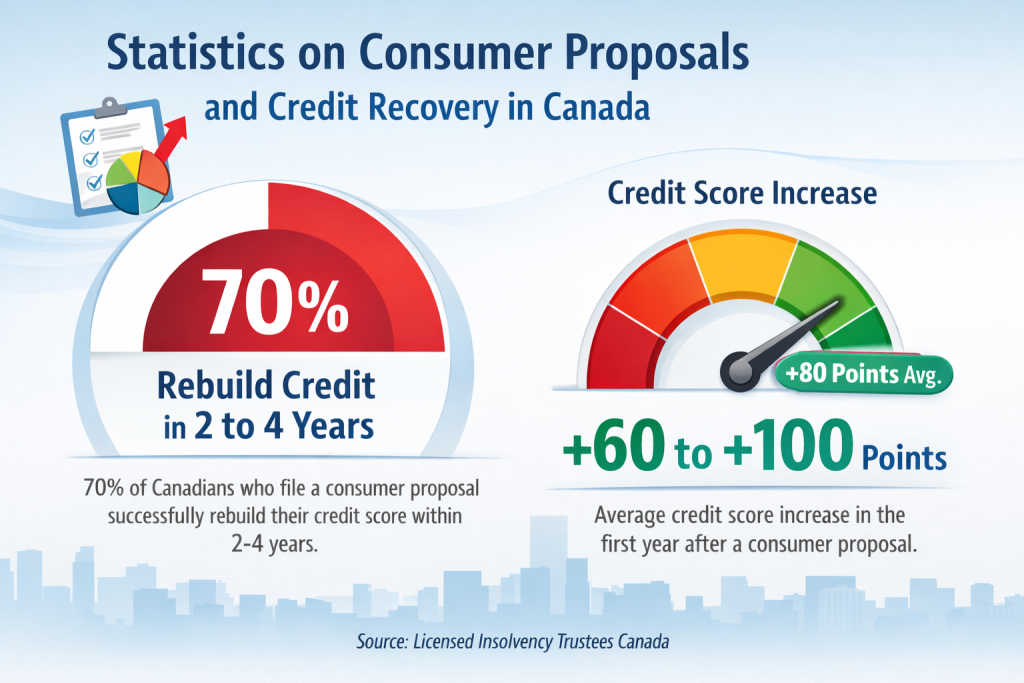

How Long Does it Take to Rebuild Your Credit After a Consumer Proposal?

Once your consumer proposal is completed, you’ll be eager to rebuild your credit. Here’s how you can recover your credit score and start improving it:

1. Make Timely Payments

After your proposal is completed, it’s essential to continue making timely payments on any existing debts. Paying on time will help demonstrate financial responsibility and aid in the recovery of your consumer proposal credit score.

- On-Time Payments Matter: Consistently paying your bills on time helps to rebuild trust with creditors and credit bureaus.

2. Use Credit Responsibly

Consider applying for a secured credit card once your consumer proposal is finished. This allows you to start building positive credit history while controlling your spending.

- Low Credit Utilization: Aim to use no more than 30% of your available credit. Higher utilization can hurt your credit score.

- Pay in Full: Always pay off your balance in full to avoid interest charges and demonstrate responsible credit management.

3. Regularly Check Your Credit Report

Check your credit report regularly to ensure that the consumer proposal is removed after 3 years. If any errors or discrepancies are found, report them immediately to the credit bureaus.

- Monitor Progress: Stay updated on how your credit rating evolves after the R7 status is removed.

How Long Does It Take to Recover Your Credit Score After a Consumer Proposal?

The timeline to recover your credit score can vary. For many people, it takes several months to a couple of years to rebuild their credit after a consumer proposal.

- Factors for Recovery:

- Starting Credit Score: The higher your starting score, the quicker you may recover.

- New Credit Accounts: Opening a new credit card or loan, when done responsibly, can help improve your score.

Tips to Speed Up Recovery:

- Keep Balances Low: Maintain a low debt-to-income ratio to show financial stability.

- Use Credit Wisely: Start building credit with secured cards or small loans that you repay on time.

Conclusion

A consumer proposal can be a great option for settling debts, but it does affect your credit score. The impact is significant but temporary, and with responsible financial behavior, your credit score can improve after the proposal is completed.

Remember that rebuilding your credit takes time and patience. Keep making timely payments, use credit responsibly, and regularly check your credit report to monitor progress. With these steps, you can recover your credit and move forward toward a healthier financial future.