Managing debt can feel like an overwhelming challenge, especially when balancing multiple credit cards, loans, and bills. A Debt Management Plan (DMP) can offer a structured approach to help you regain control and pay off your debts faster. However, with so many options available, how do you find the right DMP for your unique situation?

In this article, we’ll dive deep into what Debt Management Plans are, how they work, and what to look for when choosing the best one for you.

What is a Debt Management Plan (DMP)?

A Debt Management Plan is a structured repayment plan that allows you to consolidate multiple debts into a single monthly payment. By enrolling in a DMP, you work with a credit counselling agency to negotiate lower interest rates, reduced monthly payments, and sometimes even debt forgiveness.

Key Features of a DMP:

- Single Monthly Payment: Instead of juggling multiple creditors, you make one monthly payment to a credit counselling service, which then distributes the funds to your creditors.

- Negotiated Terms: The credit counsellor negotiates with your creditors to reduce interest rates and eliminate fees, making repayment more manageable.

- Fixed Timeframe: DMPs typically last between 3 to 5 years, and once completed, your debts are considered paid in full.

A DMP can be a game-changer, but it’s important to understand how it works before committing.

How Does a Debt Management Plan Work?

- Assessment: You begin by meeting with a certified credit counsellor who assesses your financial situation, including income, expenses, and outstanding debts.

- Negotiation: The counsellor negotiates with your creditors to lower interest rates and waive fees.

- Payment Plan: Based on the negotiations, you agree on a fixed monthly payment that you can afford. This payment goes to the counselling agency, which pays your creditors.

- Tracking Progress: Throughout the plan, the credit counselling service monitors your progress, ensuring that you’re sticking to the plan and making regular payments. For this service, you can get help from Kunjar Sharma & Associates Inc.

Debt Management Strategies: How to Choose the Right Plan

Choosing the right debt management strategy depends on your financial goals and situation. Here are a few tips to help you determine the best approach:

1. Evaluate Your Debts

- Secured vs. Unsecured Debt: Secured debts (like mortgages) might not be included in a DMP, while unsecured debts (credit cards, medical bills) are typically eligible.

- Total Amount of Debt: If your debts exceed a certain threshold, a DMP might be more effective than attempting to pay off each debt individually.

2. Consider Other Debt Solutions

- Debt Settlement: If your debts are significantly high, you might want to explore debt settlement, where creditors agree to accept less than what you owe. However, this can negatively impact your credit score.

- Bankruptcy: If your debt is unmanageable and a DMP doesn’t seem like the right fit, bankruptcy might be the last resort. It’s essential to consult with a financial expert before making this decision.

User Insights: What Real People Say About Debt Management Plans

Debt Management Services: Benefits and Drawbacks

Benefits of Debt Management Services:

- Lower Monthly Payments: The primary benefit is reduced monthly payments, making it easier to manage your finances.

- Reduced Interest Rates: Negotiated interest rate reductions can save you a significant amount of money over time.

- Debt-Free Future: The structured nature of DMPs helps you stay on track and work towards becoming debt-free.

Drawbacks of Debt Management Services:

- Impact on Credit Score: Although you’ll likely see your credit score improve after completing the plan, being enrolled in a DMP can initially cause a slight drop.

- No Access to Credit: During the term of your DMP, you might not be able to open new credit accounts.

- Eligibility Limitations: Some types of debt, like student loans, may not be eligible for inclusion in a DMP.

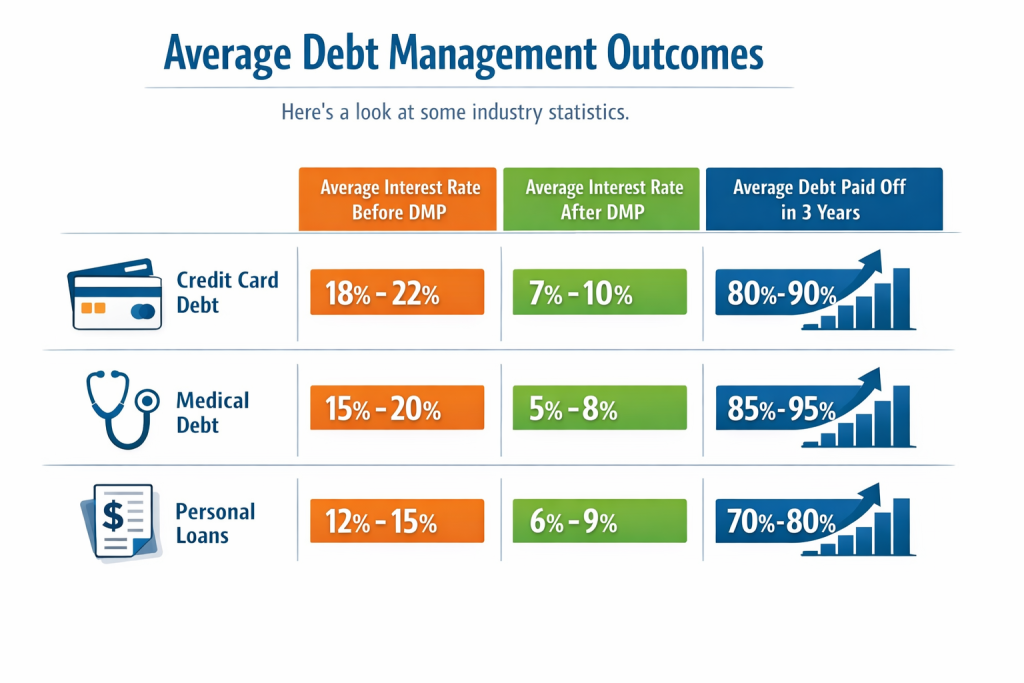

Data Insights: Average Debt Management Outcomes

Here’s a look at some industry statistics:

As you can see, debt management plans can significantly reduce the amount of interest you pay over time and help you pay off your debt faster.

Conclusion: Is a Debt Management Plan Right for You?

Debt management plans are a powerful tool for those seeking to regain control over their finances. By consolidating multiple debts into one manageable monthly payment, you can reduce stress and focus on paying off your debt without the overwhelming burden of high interest rates.

Remember to consider your financial situation carefully and consult with a certified credit counsellor before committing to a DMP. By understanding your options and choosing the right plan for you, you’ll be on your way to a debt-free future.