Feeling overwhelmed by debt? You’re not alone; many Canadians struggle with managing credit card balances, loans, and mortgages. But the good news is, with the right strategies, you can take control of your financial future. In this guide, we’ll break down proven methods for reducing debt, improving cash flow, and ultimately achieving financial freedom. No more stress, no more sleepless nights, just actionable steps you can take right now.

1. Understanding Debt Management

Managing debt is more than just paying off outstanding balances — it involves a comprehensive approach to restructuring your finances, understanding where your money goes, and committing to long-term solutions. Effective debt management goes hand in hand with a well-crafted plan, so let’s first break down what “debt management” means in the Canadian context.

What is Debt Management?

Debt management refers to a process where individuals or businesses organize and prioritize their debts in a way that maximizes their ability to pay them off. The primary goal is to avoid defaulting on loans and to manage outstanding debts so that they are paid off in a structured and timely manner.

2. How to Manage Money and Get Out of Debt: Budgeting & Saving

Getting out of debt isn’t just about reducing what you owe; it’s also about managing your money effectively to build long-term financial health. Here’s how to start:

Create a Realistic Budget

Budgeting is one of the most effective tools for managing your money and paying off debt. Use a budget to track your income, expenses, and how much you are dedicating to debt repayment. A simple formula to follow is the 50/30/20 Rule:

Build an Emergency Fund

While paying off debt should be your priority, it’s also important to build a small emergency fund. This will prevent you from accumulating more debt in case unexpected expenses arise. Aim for $500–$1,000 as a starting point.

3. How to Manage Debt Problems: Key Steps

If you are struggling with debt problems, it’s important to take immediate action. Here’s a step-by-step approach to managing debt effectively:

Step 1: Assess Your Financial Situation

Before taking any action, understand exactly where you stand financially. This means gathering all your statements, credit card bills, personal loans, car loans, student loans, mortgages, and any instances of mortgage insolvency. Make a list of your debts, noting the interest rates and minimum payments for each. This gives you a clearer picture of your total debt load and helps you identify where you can start making changes.

Step 2: Create a Debt Management Plan (DMP)

A Debt Management Plan is a structured repayment strategy that helps you organize your debts. You can approach it in two main ways:

- Snowball Method: Focus on paying off the smallest debt first while making minimum payments on larger debts.

- Avalanche Method: Focus on paying off the highest-interest debts first while making minimum payments on others.

The key is to stick to your plan. Both strategies are effective, but the avalanche method may save you more money in the long run because it reduces the amount of interest you pay over time.

Step 3: Cut Unnecessary Expenses

While you work on paying down your debts, it’s essential to limit your spending. Review your budget and identify areas where you can cut back. For example:

- Dining Out: Reduce spending on restaurants and coffee shops.

- Subscriptions: Cancel any subscriptions or memberships you don’t need.

- Impulse Purchases: Consider implementing a “cool-off” period before making big purchases.

Use any savings you generate to accelerate your debt repayment process.

Step 4: Negotiate with Creditors

It’s worth reaching out to your creditors to negotiate lower interest rates or more favorable payment terms. Many creditors are willing to work with you if you demonstrate a commitment to paying off your debt. If you’re struggling to make payments, you can also ask for an extended payment plan.

Step 5: Explore Debt Consolidation

Debt consolidation involves combining multiple debts into one, typically with a lower interest rate. This can simplify payments, reduce interest, and help you pay off debt faster. You can consolidate debt through a personal loan, a home equity loan, or by using a credit card with a 0% balance transfer offer.

Step 6: Consider Credit Counseling

If you’re feeling overwhelmed, the credit counseling service can help. It can guide you through your options and help you create a plan to regain control of your finances.

4. What Canadians Are Saying About Debt Management

One Reddit user, “CanuckBudgeter”, shared their success with debt consolidation on r/PersonalFinanceCanada: “Debt consolidation helped me reduce my payments and keep track of everything in one place. It made things so much easier, and I can finally see the light at the end of the tunnel.”

This method can simplify debt repayment and lower interest rates, helping Canadians regain control of their finances.

5. The Importance of Seeking Professional Help

Sometimes, debt problems can become too complicated to handle on your own. This is where debt management professionals come in. If you feel like you’re reaching your limit or facing insurmountable debt, don’t hesitate to reach out to financial advisors or certified credit counselors.

Debt management professionals can:

- Help you develop a personalized plan based on your unique financial situation.

- Provide support with negotiating with creditors.

- Offer guidance on avoiding common mistakes that can make debt worse.

If you’re looking for expert advice and support, apply to Kunjar Sharma & Associates Inc. for professional debt management assistance.

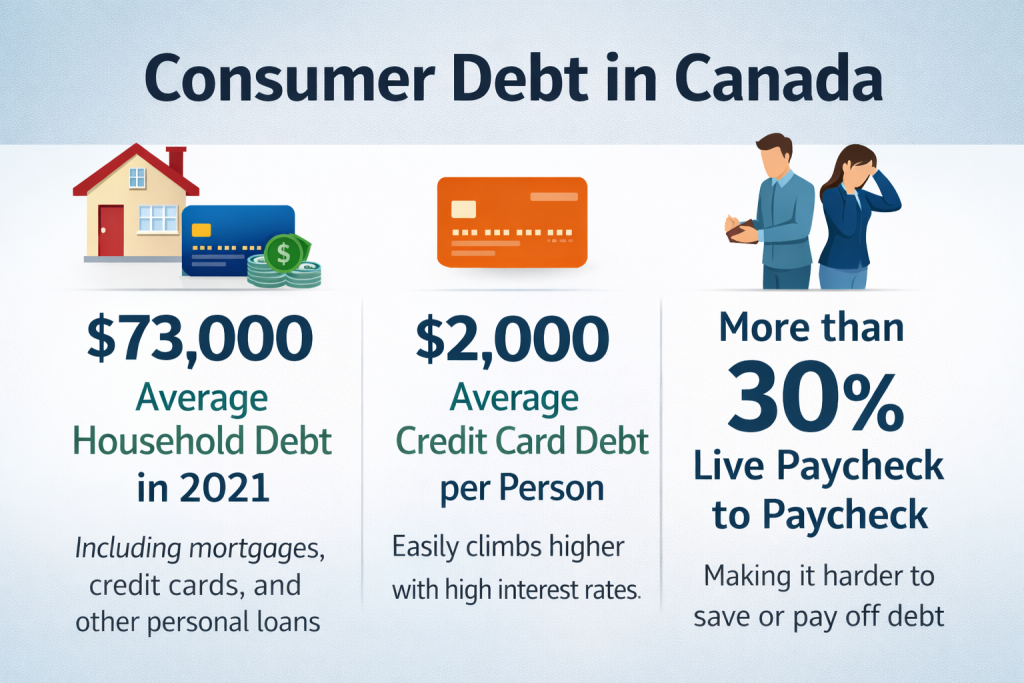

6. Key Statistics on Debt in Canada

Understanding the broader picture of debt in Canada can give you insight into your personal financial situation. Here are some relevant statistics:

Final Thoughts

Successfully managing debt in Canada requires a comprehensive approach, starting with an honest assessment of your financial situation, followed by a well-thought-out plan and the use of available resources. Whether you use the snowball method, consult a debt counsellor, or explore consolidation options, the key is to stay committed and seek help when needed.

Start today, use the tips and strategies provided in this guide, and soon you’ll be on your way to managing your debt and improving your financial future.