Running a business comes with its fair share of challenges. Financial difficulties, however, can be particularly distressing. Whether due to poor cash flow management, unforeseen expenses, or external market forces, financial struggles can threaten a company’s viability. If you’re a business owner facing such challenges, there are steps you can take to protect your business, mitigate risks, and explore options for restructuring.

This article will explore practical strategies and expert insights to help protect your business from financial difficulties, ensuring long-term survival and recovery.

1. Assess Your Financial Situation: The Foundation of Protection

Before you can take proactive steps, it’s crucial to assess the full extent of your financial difficulties. Often, business owners avoid confronting financial challenges due to fear or uncertainty. However, understanding the scope of the issue is the first step toward finding solutions.

Key Steps to Assess Your Financial Health:

- Review Cash Flow Statements: A poor cash flow can lead to liquidity issues, which means you may struggle to pay bills or meet payroll.

- Examine Your Balance Sheet: Check for assets versus liabilities. Do your liabilities outweigh your assets? Are there assets that could be liquidated if needed?

- Track Expenses: Look for areas where you can cut unnecessary expenses without jeopardizing business operations.

- Identify Debt Patterns: Are you accumulating debt faster than you’re able to pay it off? How much of your income is tied up in servicing debt?

Tools to Help Assess Financial Health:

- Financial Dashboard Software: Use tools like QuickBooks or Xero to get a real-time overview of your business’s financial health.

- Key Performance Indicators (KPIs): Metrics like current ratio, quick ratio, and debt-to-equity ratio can provide insights into your financial stability.

2. Explore Debt Restructuring Options: Consumer Proposal or Bankruptcy

If your business has significant outstanding debts, debt restructuring may be an option. In Ontario, businesses have a variety of options to manage debt, including consumer proposals or formal bankruptcy.

Consumer Proposals for Businesses

A consumer proposal allows businesses to negotiate with creditors to pay off a portion of their debt over a manageable period (usually 3 to 5 years), rather than facing liquidation. It can be an ideal option if the business wants to continue operations but needs relief from overwhelming debt. This process involves a Licensed Insolvency Trustee (LIT) who helps you create the proposal and negotiate with creditors.

Benefits of a Consumer Proposal:

- Protection from creditors: Your creditors cannot take legal action or collect debts once a consumer proposal is filed.

- Preserve your assets: Unlike bankruptcy, which may require asset liquidation, a consumer proposal may allow you to retain your business assets.

- Reduce debt: You may only need to repay a portion of the debt owed, easing your financial burden.

However, a consumer proposal does have eligibility requirements, and not all businesses qualify. A Licensed Insolvency Trustee can help assess your business’s specific situation and determine if this option is suitable.

Bankruptcy as a Last Resort

If debt restructuring options like a consumer proposal are unfeasible, bankruptcy may be the last option for businesses. While bankruptcy can provide a fresh start by discharging debt, it involves the liquidation of assets, which could mean the end of your business. However, in some cases, restructuring through bankruptcy can also provide an opportunity for the business to emerge in a stronger financial position.

3. Strengthen Cash Flow Management: A Key Pillar of Protection

One of the most effective ways to protect your business during financial difficulties is by actively managing your cash flow. Ensuring you have enough liquidity to cover short-term obligations is crucial to maintaining daily operations and avoiding a downward financial spiral.

Strategies for Improving Cash Flow:

- Invoice Promptly: Avoid delays in invoicing. Use automated invoicing software to send invoices as soon as a service or product is delivered.

- Negotiate Better Payment Terms with Vendors: Try to extend your payment terms to improve cash flow. Vendors may be willing to grant you 30, 60, or even 90 days to pay instead of 15 or 30.

- Offer Discounts for Early Payments: Incentivize clients to pay early by offering a small discount, which can quickly improve your cash position.

- Implement Strict Credit Control: Avoid granting credit to customers with poor payment histories. Regularly review outstanding payments and follow up on overdue invoices.

- Consider Alternative Financing Options: Explore short-term financing options like business lines of credit or invoice factoring to manage cash flow gaps.

4. Cost-Cutting Without Jeopardizing Growth

Cutting costs during difficult financial times is necessary, but it must be done carefully. Overzealous cost-cutting measures can harm your business’s growth prospects. Instead, target areas that provide the greatest financial relief without compromising the integrity of your business operations.

Cost-Cutting Strategies:

- Outsource Non-Core Functions: If you’re facing cash flow issues, consider outsourcing functions like IT support, HR, or marketing rather than hiring full-time employees.

- Renegotiate Contracts: Review your contracts with suppliers and service providers. Renegotiating terms can often provide immediate financial relief.

- Reduce Inventory: Excess inventory ties up cash. Evaluate your stock levels and reduce unnecessary inventory.

- Implement Remote Work: If feasible, encourage employees to work remotely to reduce office-related costs (e.g., rent, utilities).

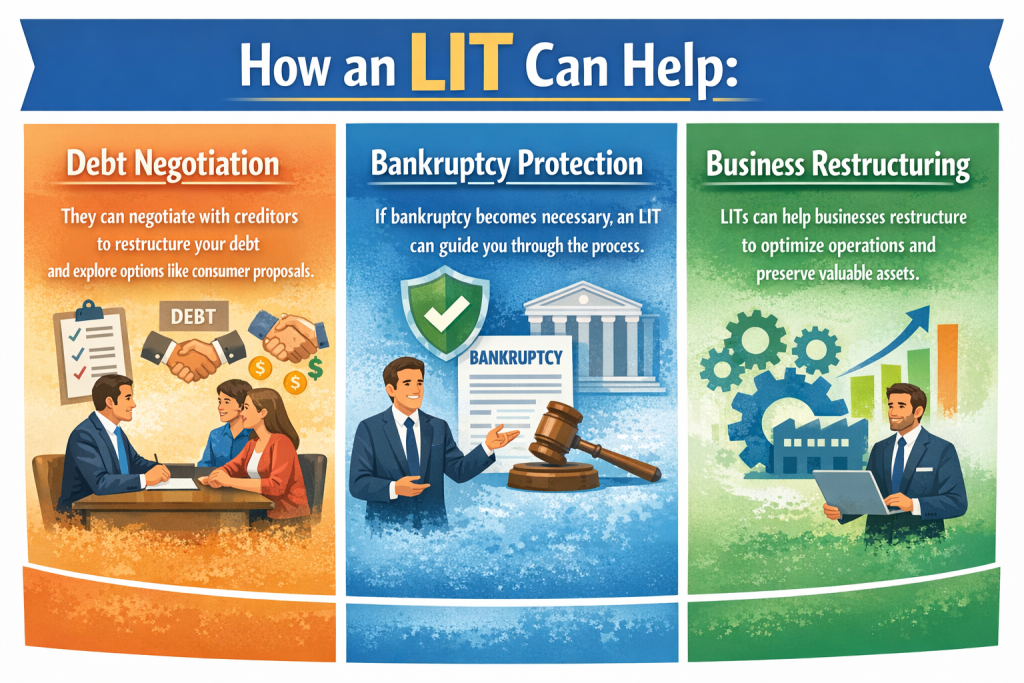

5. Seek Professional Advice from a Licensed Insolvency Trustee

When facing severe financial distress, seeking expert guidance from a Licensed Insolvency Trustee (LIT) is essential. They are government-regulated professionals with the knowledge and experience to help businesses navigate financial difficulties.

6. Consider Alternative Funding Options

If your business is struggling with cash flow, it might be time to explore external funding options to provide some breathing room. Consider these options:

Funding Sources:

- Government Grants and Subsidies: There may be government programs that offer financial assistance to businesses in distress, especially during times of economic hardship.

- Private Lenders: Explore private lenders that provide financing to businesses with poor credit histories.

- Venture Capital or Angel Investors: If your business shows high growth potential, you might attract venture capital or angel investors looking to inject capital in exchange for equity.

7. Legal Protection: Preventing Creditors from Seizing Assets

During financial difficulties, it’s essential to know your rights and the protections available to your business. Ontario has laws that protect businesses from creditors through various mechanisms, such as:

- The Bankruptcy and Insolvency Act (BIA): This act governs bankruptcy and insolvency proceedings and offers protections against aggressive creditor actions.

- Corporate Protection Laws: Certain corporate structures (e.g., corporations) offer limited liability protection, meaning your personal assets cannot be seized to pay off business debts.

Protecting Personal Assets:

- Incorporation: If you are operating as a sole proprietorship, consider incorporating your business to separate your personal and business assets legally.

- Trust Accounts: Using trust accounts can help protect customer funds from creditors.

Conclusion: Navigating Financial Difficulties with a Plan

Financial difficulties don’t have to mean the end of your business. With a structured approach, careful planning, and professional guidance, you can not only protect your business but also emerge stronger on the other side. From evaluating your financial health to leveraging debt restructuring options and exploring funding, there are several ways to manage business challenges effectively.

Taking proactive steps—such as seeking advice from a Licensed Insolvency Trustee—can give your business the best chance of recovery and long-term success.

For immediate support, consider reaching out to a licensed professional who can guide you through these difficult financial times.