Few worries weigh more heavily on someone struggling with debt than the fear of being arrested for it. Aggressive collection calls, threatening letters, and court summons can make the situation feel criminal, even when it isn’t. So if you’ve found yourself searching whether unpaid debt could land you behind bars, here’s the direct answer first: no, you cannot be sent to jail in Canada simply for being unable to pay your debts.

That short answer, though, doesn’t tell the full story. There are real consequences for ignoring debt, a few narrow situations where legal trouble can arise, and, most importantly, a clear set of options available to anyone facing serious financial pressure. This article walks through all of it, so you understand exactly where you stand and what to do next.

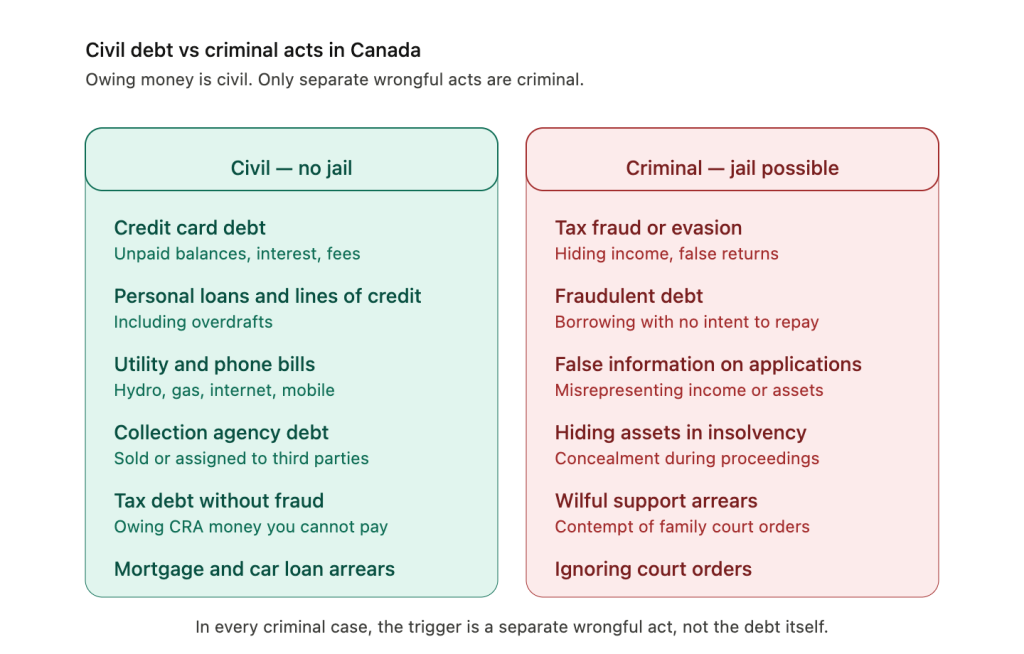

The Short Answer: Debt Itself Is Not a Criminal Offence

Canada abolished imprisonment for civil debt in the 19th century. Today, the inability to repay money you owe, whether it’s a credit card, a personal loan, a line of credit, a utility bill, or a debt sold on to a collection agency, is a civil matter, not a criminal one. Creditors have legal options to recover what they’re owed, but those options run through civil courts, not the criminal justice system.

The framework that governs personal and business insolvency in Canada is the federal Bankruptcy and Insolvency Act (BIA). It’s a civil statute, designed to balance the rights of debtors and creditors and to give people a structured path out of financial distress. Nothing in the BIA puts a person in jail for owing money.

That said, there are a few specific situations where debt-related conduct can lead to legal – and in rare cases, criminal – consequences. Those are worth understanding clearly.

When Debt-Related Issues Can Lead to Legal Trouble

The exceptions below all share one thing in common: it isn’t the debt itself that’s the problem. It’s a separate legal act tied to the debt.

Tax fraud or evasion. Owing money to the Canada Revenue Agency (CRA) is not a crime. Deliberately misrepresenting your income, hiding assets, or filing false returns to avoid taxes you owe is a criminal offence under the Income Tax Act. The trigger is intentional deception, not the unpaid balance.

Unpaid child or spousal support. Family support obligations are treated very differently from consumer debts. In Ontario, the Family Responsibility Office (FRO) enforces support orders and has powerful tools at its disposal, including suspending driver’s licences, garnishing income, restricting passports, and, in cases of repeated wilful non-payment, seeking a contempt of court finding that can result in imprisonment. Again, it’s the violation of a court order that triggers consequences, not the debt itself.

Contempt of court. If a creditor has obtained a judgment against you and you ignore a related court order (for example, failing to attend a judgment debtor examination), a court can hold you in contempt. The penalty isn’t for owing money; it’s for disregarding the court.

Fraud. Taking on debt with no intention of repaying it, providing false information on a credit application, or hiding assets during insolvency proceedings can all constitute fraud under the Criminal Code. These are deliberate acts of deception, not financial hardship.

In every case, the legal exposure comes from a separate wrongful act, not from being unable to pay.

What Actually Happens When You Don’t Pay Your Debt

For most people, the real question behind “can I go to jail?” is “what will actually happen?” Understanding the typical progression makes it far easier to plan a response. Here is how unpaid consumer debt usually unfolds in Canada.

Late fees and credit damage. As soon as a payment is missed, late fees and additional interest start to accrue. Missed payments are reported to Equifax and TransUnion, and they begin to damage your credit score.

Internal collections. The original creditor’s collections team will start calling and writing. At this stage, most lenders are open to discussing hardship arrangements or modified payment plans.

Third-party collection agency. If the account remains unpaid, the creditor will typically either assign or sell the debt to a collection agency. This is where pressure tactics often intensify, and where many of the threats people fear, including, in some cases, illegal threats of jail or arrest, tend to surface.

Civil lawsuit. If the debt remains unresolved, a creditor can sue. In Ontario, claims of up to $35,000 are heard in Small Claims Court. Larger amounts go to the Superior Court of Justice.

Judgment. If the creditor wins (or you don’t respond and lose by default), the court issues a judgment. With a judgment in hand, the creditor can pursue:

- Wage garnishment, subject to provincial limits on how much of your income can be taken

- Bank account seizure

- Liens on real property, such as a home

Long-term credit damage. Negative entries — including judgments, collection accounts, and consumer proposals or bankruptcies — generally remain on your Canadian credit report for six to seven years, depending on the type and the province.

One important point that’s often overlooked: most consumer debts in Ontario become statute-barred after two years of inactivity, under the Limitations Act, 2002. That means if you haven’t acknowledged the debt or made a payment in that period, the creditor loses the right to sue you for it. The debt doesn’t disappear from your credit report, and a collection agency can still attempt to recover it, but they cannot enforce it through the courts. Acknowledging the debt — even verbally — can restart the clock, so it’s worth being aware of before responding to old collection calls.

Your Rights When Dealing with Collection Agencies in Ontario

Because so much of the fear around debt and jail comes from collection agency tactics, it’s worth being clear on what these agencies are legally allowed to do, and what they aren’t.

In Ontario, collection agencies are regulated under the Collection and Debt Settlement Services Act. Among other things, they are prohibited from:

- Threatening you with arrest, jail, or criminal charges (this is illegal, and a clear sign of an unscrupulous operator)

- Calling you before 7 a.m. or after 9 p.m. on weekdays, before 1 p.m. or after 5 p.m. on Sundays, or at all on statutory holidays

- Contacting your employer except to confirm employment, address, or telephone number

- Contacting your family, friends, or neighbours about your debt (other than to obtain your contact information, in limited circumstances)

- Using threatening, profane, intimidating, or coercive language

- Continuing to contact you after you’ve requested in writing that they communicate only through your legal representative

If a collection agency threatens you with jail, that’s not just unprofessional, it’s a regulatory violation. You can file a complaint with the Government of Ontario, which oversees collection agencies in the province.

What to Do Instead of Ignoring the Debt

Knowing you can’t be jailed for debt is reassuring. But ignoring debt is rarely the right response: the longer you leave it, the fewer options remain, and the more aggressive enforcement becomes. The good news is that Canada has a well-developed framework of legitimate debt-relief options, ranging from informal arrangements to formal legal solutions.

Negotiate directly with creditors. Many lenders will agree to revised payment terms, interest reductions, or temporary forbearance, particularly if approached early. This works best for short-term hardships rather than long-term insolvency.

Debt consolidation. Combining several high-interest debts into a single lower-interest loan can simplify repayment and reduce overall interest costs. It works best when your credit is still reasonably strong.

Credit counselling. A qualified financial counsellor can help you build a realistic budget, review your debts, and identify the right path forward. Kunjar Sharma & Associates offers credit counselling services delivered by federally licensed professionals.

Debt management plan. Often arranged through credit counselling, a debt management plan consolidates unsecured debts into a single monthly payment, often with reduced or waived interest. Our detailed guide on debt management plans explains how the process works and who it’s best suited for.

Consumer proposal. A consumer proposal is a legally binding agreement administered by a Licensed Insolvency Trustee that allows you to repay a portion of what you owe over up to five years. Once filed, it immediately stops collection calls, wage garnishments, and lawsuits. For many people, it offers significantly more debt reduction than a debt management plan, while avoiding the more serious consequences of bankruptcy.

Personal bankruptcy. Where no other option is realistic, personal bankruptcy provides a legal fresh start. It immediately halts creditor actions and discharges most unsecured debts, in exchange for the surrender of certain non-exempt assets and a defined process supervised by a Licensed Insolvency Trustee. It’s a last resort, but for many people in genuinely insurmountable financial situations, it’s the right one.

Why Acting Early Matters

The single most important factor in resolving debt successfully is timing. Early action almost always produces better outcomes than late action.

When debts are still with the original creditor, you have the most flexibility to negotiate. Once a debt has been sold, sued on, or turned into a judgment, your options narrow and the cost of resolving it climbs. Wage garnishments, bank account seizures, and liens are not inevitable, but avoiding them depends on engaging with the situation before the creditor takes those steps.

It’s also worth noting that Licensed Insolvency Trustees are the only professionals in Canada legally authorized to administer Consumer Proposals and Bankruptcies under the BIA. They are federally regulated by the Office of the Superintendent of Bankruptcy Canada and held to strict professional standards. A free initial consultation with an LIT typically clarifies which options are realistic for your situation, what the costs and consequences are, and what the next steps look like, with no obligation to proceed.

Frequently Asked Questions

Can you go to jail for credit card debt in Canada? No. Credit card debt is a civil matter. A creditor can sue you, obtain a judgment, and pursue wage garnishment or other enforcement, but you cannot be imprisoned for being unable to pay it.

Can a collection agency send me to jail? No, and threatening you with jail is illegal in Ontario and across Canada. Collection agencies have no power to arrest you or initiate criminal proceedings.

Can you go to jail for not paying CRA taxes? Not for being unable to pay. The CRA has wide powers to collect, including garnishment and asset seizure, but criminal prosecution is reserved for tax fraud or evasion, that is, intentional deception.

What happens if I just ignore my debt in Canada? The debt typically progresses through internal collections, sale to a third-party agency, possible legal action, judgment, and enforcement (wage garnishment, bank seizure, liens). Your credit will be seriously damaged for several years.

Does debt follow you across provinces or out of Canada? Yes. Moving within Canada doesn’t erase debt, and creditors can pursue judgments across provincial lines. International enforcement is more complex but not impossible, particularly within reciprocal jurisdictions.

How long does an unpaid debt stay on my credit report? Most negative information remains on a Canadian credit report for six to seven years from the date of last activity, depending on the type of entry and the province.

The Bottom Line

The fear of jail keeps far too many Canadians paralyzed when they should be taking action. The legal reality is straightforward: in Canada, you cannot be imprisoned for being unable to pay your debts. What you can face is a civil enforcement process that becomes harder to manage the longer it’s left.

If you’re feeling overwhelmed by debt, the most productive next step is rarely to keep worrying about jail, it’s to speak with a professional who can clarify exactly where you stand and what your options are.

A free, confidential consultation with a Licensed Insolvency Trustee at Kunjar Sharma & Associates can help you understand your situation and choose the path forward that’s right for you. With more than 40 years of experience and 6,000+ proposals filed, our team has helped thousands of individuals, families, and business owners across the GTA move from financial distress to a brighter financial future.

You don’t go to jail for debt in Canada. But you also don’t have to live with the weight of it. The right path forward starts with a conversation.