For homeowners facing serious financial difficulty, no question matters more than what happens to the family home. The fear of losing it often delays the very action that could resolve the situation, leaving people stuck in a holding pattern of growing debt, anxiety, and dwindling options. So it’s worth answering the question directly: yes, in many cases you can keep your house when you declare bankruptcy in Canada. Whether you actually do, however, depends on a number of specific factors, and understanding them is the first step to making the right decision.

This article walks through how home equity is treated in a Canadian bankruptcy, when keeping the home is realistic and when it isn’t, and why a Consumer Proposal is often the better route for homeowners who want to protect their property. The rules vary by province and personal circumstance, but the underlying logic is the same across Canada.

The Short Answer: It Depends on Your Equity

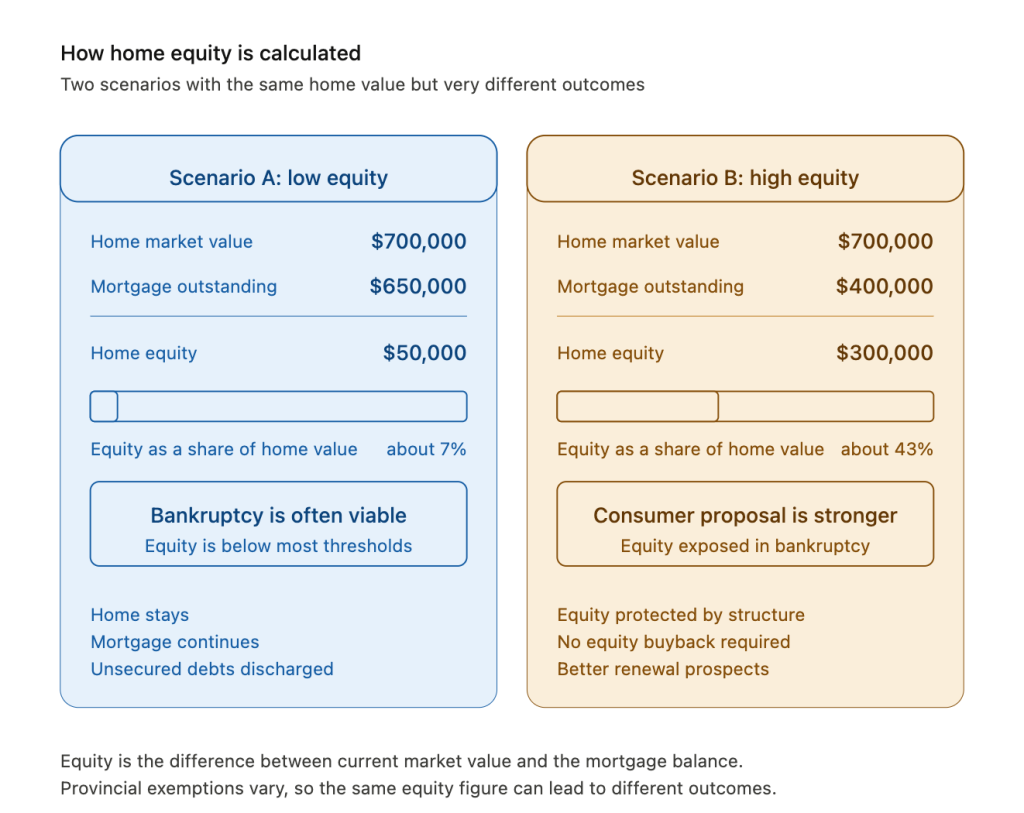

Bankruptcy in Canada doesn’t automatically mean losing your home. What matters is how much equity you have in the property, in other words, the difference between the home’s current market value and the amount still owed on the mortgage.

A simple example. If your house is worth $700,000 and you owe $650,000 on the mortgage, you have $50,000 in equity. If your house is worth $700,000 and you owe $400,000, you have $300,000 in equity. Those two situations are treated very differently in bankruptcy, because Canadian bankruptcy law allows certain types and amounts of property to be retained, while assets above defined thresholds are typically realised for the benefit of creditors.

The Licensed Insolvency Trustee handling the bankruptcy works through this calculation early in the process. The outcome determines whether keeping the house is straightforward, possible with conditions, or not realistic without an alternative approach.

How Home Equity Is Treated in a Canadian Bankruptcy

When you file for bankruptcy in Canada under the federal Bankruptcy and Insolvency Act, your non-exempt assets are assigned to the Trustee, who then realises them for distribution to creditors. Each province sets its own rules on which assets are exempt and up to what value, and these provincial exemptions interact with the federal bankruptcy framework.

For a principal residence specifically, the picture varies meaningfully across the country.

In Alberta, there is a homestead exemption of $40,000 of equity in a principal residence. In British Columbia, the exemption is $12,000 in Greater Vancouver and Greater Victoria, and $9,000 elsewhere in the province. In Manitoba, it’s $2,500. In Saskatchewan, $32,000. Ontario, Quebec, and the Atlantic provinces generally do not have a specific home equity exemption; instead they apply general personal property exemptions that don’t typically protect significant home equity.

What this means in practice. If you live in Ontario and your home has substantial equity, that equity is in principle available to your creditors through the bankruptcy. The Trustee may require the equity to be realised, either through a sale of the home or through a payment arrangement that compensates creditors for an equivalent amount.

If you have little or no equity, however, the Trustee has nothing meaningful to realise, and keeping the home through bankruptcy becomes much more straightforward, provided you can keep up with the mortgage payments.

When Keeping the House Through Bankruptcy Is Realistic

Three conditions tend to make it possible to keep your home through a Canadian bankruptcy.

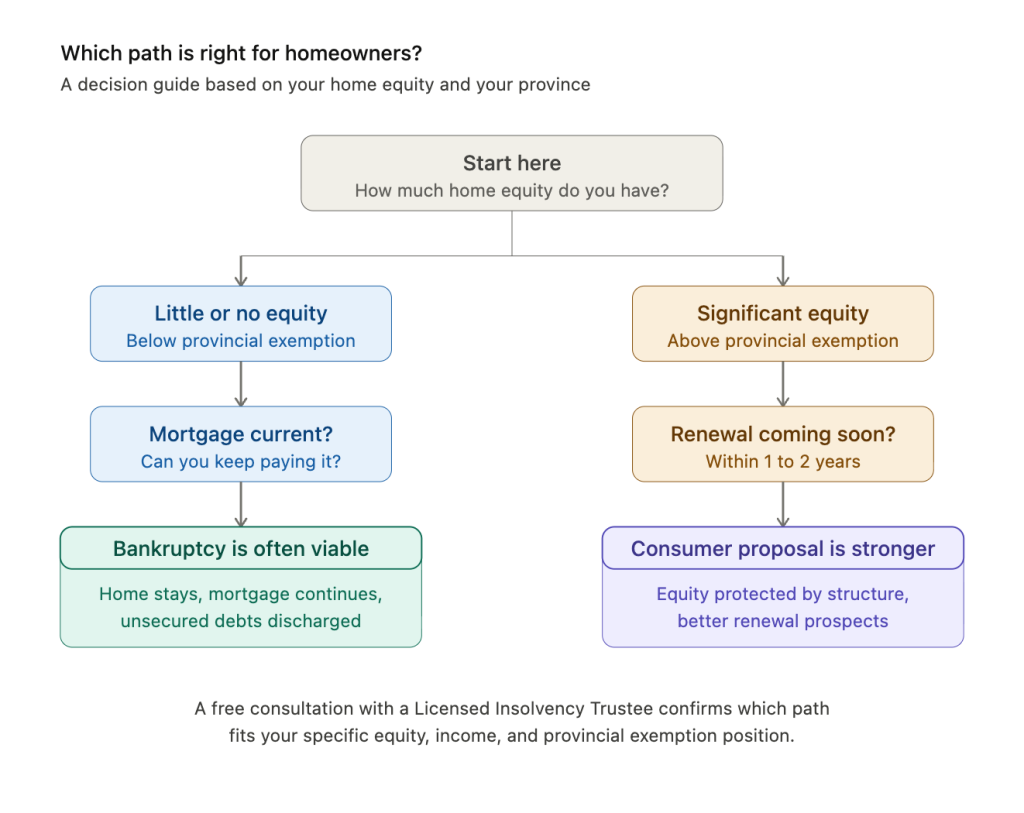

1. Low or no equity. If the equity in your home is at or below your provincial exemption (or genuinely close to zero in provinces without a meaningful homestead exemption), the Trustee usually has no reason to realise the property. The mortgage continues, and the bankruptcy proceeds without affecting the home directly.

2. The mortgage is current and you can keep paying it. Bankruptcy doesn’t discharge a mortgage in the same way it discharges unsecured debt like credit cards or personal loans. The mortgage is secured against the property, and the lender retains the right to enforce against the home if payments stop. Keeping the house means continuing to pay the mortgage on time throughout and after the bankruptcy.

3. Your mortgage lender is willing to continue with you. Most lenders will continue an existing mortgage through a bankruptcy as long as payments are being made, but renewal at the end of the term is a separate question that often becomes the real challenge. Some homeowners find that lenders are reluctant to renew at the original rate, or at all, after a bankruptcy is recorded on their credit file. This is a major reason many Canadian homeowners explore a consumer proposal before defaulting to bankruptcy, because it generally results in a less severe credit impact and better access to mortgage products at renewal.

When all three conditions are met, the practical effect on the home of going through bankruptcy is often minimal. The house stays. The mortgage continues. The unsecured debts that were causing the financial pressure are discharged. Life on the property side of the ledger looks much the same after the bankruptcy as it did before.

When Keeping the House Becomes Difficult

Several scenarios complicate the picture and deserve specific attention.

Significant equity in a province with limited exemptions. A homeowner in Ontario with $200,000 of equity in their home cannot simply protect it by claiming a homestead exemption. The Trustee will need to address that equity in some way, either through realisation or through an arrangement where the bankrupt person (or a family member) buys the equity back from the estate. This is often workable, but it requires either liquidity or a willing third party, and the cost of buying back the equity reduces the financial benefit of the bankruptcy itself.

Falling behind on the mortgage. If mortgage payments are already in arrears or if the financial situation makes them unaffordable going forward, the lender may move to enforce against the property regardless of the bankruptcy. Bankruptcy doesn’t create the right to live in a home you can’t afford. The math has to work on a continuing basis.

Joint ownership with a non-bankrupt spouse. Where a spouse co-owns the home and is not declaring bankruptcy, only the bankrupt person’s share of the equity is potentially available to creditors. This often leads to negotiated arrangements where the non-bankrupt spouse effectively buys out the bankrupt person’s share, preserving the family home but requiring upfront capital. Whether this is feasible depends entirely on the family’s resources and willingness.

Mortgage renewal during or shortly after bankruptcy. Even when bankruptcy itself doesn’t disturb the home, the next renewal can be a flashpoint. Lenders evaluate risk at renewal, and a recent bankruptcy on file can lead to refused renewal, higher rates, or a requirement to switch to a sub-prime lender. Homeowners approaching a renewal in this window benefit from understanding how a consumer proposal can affect mortgage renewal compared with a full bankruptcy filing, because the difference in renewal outcomes can be substantial.

Why a Consumer Proposal Is Often the Better Choice for Homeowners

For most Canadian homeowners with significant equity, the practical answer is not “how do I keep the house through bankruptcy” but rather “is bankruptcy actually the right tool here at all?” Often it isn’t.

A Consumer Proposal is a legally binding agreement administered by a Licensed Insolvency Trustee under the same federal Bankruptcy and Insolvency Act that governs bankruptcy. It allows you to repay a portion of what you owe (typically 30 to 50%) over up to five years, immediately stops all collection action, and crucially, does not require the realisation of home equity in the way bankruptcy can. The home, the mortgage, and your equity remain yours throughout the proposal.

For homeowners specifically, the typical advantages of a Consumer Proposal over bankruptcy are:

- Equity in the home is protected by structure, not by exemption thresholds

- The credit impact is generally less severe and shorter-lived

- Mortgage renewal prospects are usually better

- Income is not subject to surplus income payments in the way it is during bankruptcy

- The total amount repaid is often lower than the amount that would otherwise be claimed against home equity in a bankruptcy

For homeowners with little or no equity, the calculation may flip the other way, and a personal bankruptcy can be both faster and cheaper. The right choice depends on the specifics of the equity, income, debt level, and personal goals, which is precisely the conversation a Licensed Insolvency Trustee is qualified to walk you through in a free initial consultation.

How to File for Bankruptcy and Keep Your House: The Practical Steps

If bankruptcy is genuinely the right tool and the equity picture allows for retention of the home, the practical steps are as follows.

Step 1: Get a current valuation. Before any decision is made, the Trustee needs an accurate picture of the home’s market value. This is usually established through a professional appraisal or, in some cases, comparable sales.

Step 2: Confirm the mortgage balance and standing. The remaining mortgage principal, the current payment status, and the term remaining all feed into the equity calculation and into the assessment of whether the mortgage is sustainable through and beyond the bankruptcy.

Step 3: Calculate net equity. Market value minus mortgage balance minus realisation costs (legal fees, real estate commission, and similar) gives the net equity figure that the Trustee works from.

Step 4: Evaluate the equity position against your provincial exemptions. This is where the geography matters. The same equity figure can produce very different outcomes in Alberta versus Ontario.

Step 5: Identify the source of any equity buyback. If the equity exceeds the exemption and you want to keep the home, the equity will typically need to be paid into the estate. Funds may come from a family member, a refinancing, or a structured payment plan with the Trustee. This step is where many homeowners discover that a Consumer Proposal would actually have been the more economical route.

Step 6: File and continue mortgage payments uninterrupted. Once the path is clear, the bankruptcy is filed, an automatic stay halts unsecured creditor action, and the mortgage continues to be paid on schedule.

Step 7: Plan for renewal. Well before any upcoming mortgage renewal, work with the Trustee or a mortgage broker who understands post-bankruptcy lending to position the renewal as cleanly as possible.

This sequence is straightforward in concept but full of judgment calls in practice, which is why every reputable Trustee in Canada offers a free initial consultation to walk through it before any filing is made.

Frequently Asked Questions

Can you declare bankruptcy and keep your house in Canada? Yes, in many cases. Whether you can depends primarily on the amount of equity in the home, the province you live in, and your ability to keep up with the mortgage. Homes with little equity are typically straightforward to retain. Homes with significant equity in provinces with limited exemptions usually require either an equity buyback or, more commonly, a Consumer Proposal instead.

What happens to my mortgage if I file for bankruptcy? The mortgage continues. Bankruptcy doesn’t discharge a secured debt like a mortgage; it only affects unsecured debts. As long as you keep up with the payments and the lender doesn’t move to enforce, the mortgage runs through and beyond the bankruptcy normally. Renewal at the end of the term is a separate question and can be more difficult.

What if my spouse isn’t declaring bankruptcy? Where the home is jointly owned and only one spouse files, only that spouse’s share of the equity is potentially available to creditors. Common arrangements include the non-bankrupt spouse buying out the bankrupt spouse’s share to keep the home in the family, but this requires available capital.

Will I be forced to sell my home? Not automatically. The Trustee will only require sale of the home if the equity exceeds your provincial exemption and there is no other way to compensate the creditors for that excess equity. In many cases, the equity is below the threshold, or arrangements can be made to keep the home.

Is bankruptcy the only way to deal with overwhelming debt and keep my house? Almost certainly not. For most homeowners with meaningful equity, a Consumer Proposal is the stronger choice, because it protects the home equity by structure and avoids the harsher credit consequences of bankruptcy. The right answer depends on the specifics of the situation, which is what an initial consultation is designed to clarify.

The Bottom Line

Yes, you can declare bankruptcy and keep your house in Canada in many cases, but the question that really matters is whether bankruptcy is actually the right tool for your situation. For homeowners with little or no equity and a sustainable mortgage, bankruptcy can be a relatively clean route to dealing with overwhelming unsecured debt while staying in the home. For homeowners with significant equity, a Consumer Proposal is almost always the better choice, because it protects the home directly and avoids the more severe consequences of bankruptcy at mortgage renewal and beyond.

The most expensive mistake homeowners make is delaying the conversation. The longer the financial pressure builds, the more likely it becomes that mortgage payments slip, equity erodes, and the options narrow.

A free, confidential consultation with a Licensed Insolvency Trustee at Kunjar Sharma & Associates can quickly clarify whether bankruptcy or a Consumer Proposal is the right path in your specific circumstances, and what protecting your home actually requires. With more than 40 years of experience and 6,000+ proposals filed across the GTA, our team has helped thousands of Canadian homeowners restructure their finances and keep what matters most.

If you’re worried about your house, the first step isn’t to wait. It’s to find out exactly where you stand.